Who are you designing for?

In the world of behavioural economics, there exists a mythical creature - homo economicus. The homo economicus is that rare individual with the amazing ability to make only rational decisions throughout his/her life, being free from the influence of peers, emotions or even hunger. Of course homo economicus is a construct invented in the late 18th century by Adam Smith - father of economics - in an attempt to simplify human behaviour. The construct is useful in helping us understand how we should behave, but offers no insight into how we actually behave. And yet, time and again, we see many financial products designed for such a theoretical construct.

“If you look at economics textbooks, you will learn that homo economicus can think like Albert Einstein, store as much memory as IBM’s Big Blue, and exercise the willpower of Mahatma Gandhi” Richard Thaler and Cass Sunstein, Co-Authors of Nudge: Improving Decisions About Health, Wealth, and Happiness(1)

What do products designed for homo economicus look like? Let’s look at 3 examples:

1. Digital Savings Accounts.

Many of us have experienced the satisfaction of rolling up our small change, collected painstakingly over a period of time, having repeatedly tossed the coins and small bills into recycled jam jars. With the advent of digital banking products, the expectation was our behaviour would mirror homo economicus, a person who diligently keeps track of the digital version of this small change moving it regularly to an equivalent digital version of the savings jar. Let's face it, most regular people don't do that, plus the delight (from rolling that change), is virtually eliminated, no pun intended.

2. Self-Directed Investment Accounts.

Something, or usually someone causes us to purchase a stock with hopes of great returns. This prompt from the environment causes new accounts to be opened or new trades to be made. The challenge comes when markets become more volatile, or that stock they bought loses value quickly. A trusted Advisor used to execute requests to buy or sell stocks and that Advisor would remind users of their risk tolerance, or investment timelines, and provide insights which served as a type of friction against emotional decision-making. Homo economicus absent this Financial Advisor, would have the same tools as a Financial Advisor, perhaps putting a stop-loss in place or setting a target sale price, tools that help them overcome risk aversion or impatience. Unfortunately, many investors don’t do this and end up selling when markets are down, or buying when prices are too high, hurting their finances and benefiting only your company. Not a very rational outcome.

3. Life & Disability Insurance.

Awareness of the need for insurance products is highest at meaningful life events (having a child, buying a home, getting married), but understanding which product, how much to buy, and what is a great price used to be provided by a trusted Financial Advisor, or perhaps a parent or family friend who, based on their experiences would recommend options. Absent this Advisor, the cognitive load2 facing the decision-maker produces procrastination. There are so many details to consider that the individual pushes the decision-making process until later. This is not something that would happen to homo economicus.

Designing with the Mind in Mind - For Product Owners

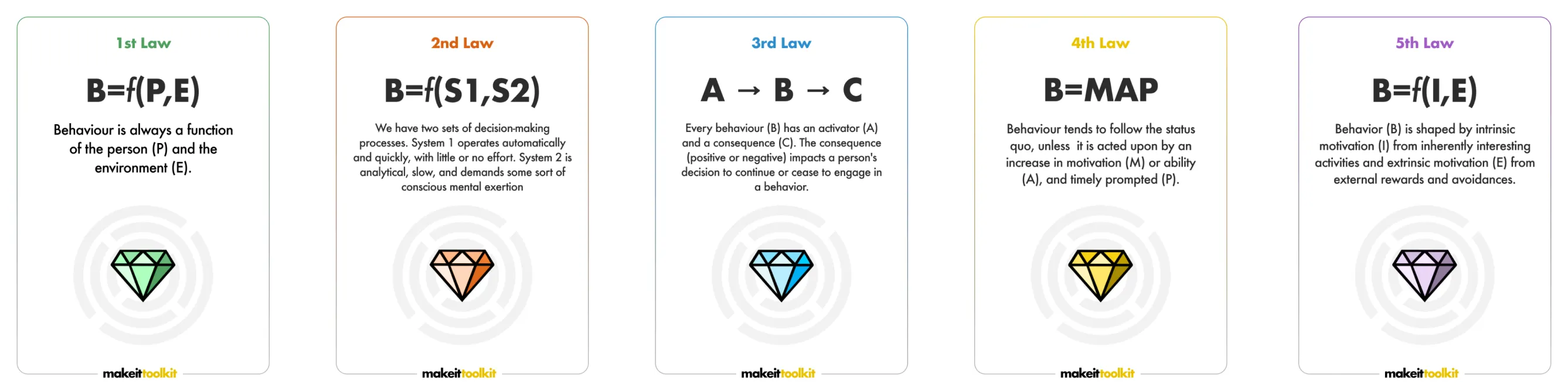

Good finance Product Owners know they need to make their products easy to use. They know that for their product to be successful, they need to consider real people, not homo economicus. We suggest thinking about the three conditions from the Fogg Model, what we’ve called the 4th Law of behaviour; Ability (is the desired behavior easy to do), Attention (does the user listen, see, and understand), and Motivation (do they want to do it).

Effectively using principles like those found in our 4th law of behaviour requires applying insights from various branches in psychology such as incentive science, habit formation, social psychology. This is why we built Makeit, to help product owners unpack behavioral science. Makeit is a practical tool that combines decades of behavioral science research, UX design best practices, and business strategy to power up your traditional design sprints.

Oh, and we made it fun! This process has been tried and tested with several finance product teams (such as Siam Commercial Bank (SCB), TMBThanachart Bank). Let’s dive into it!

Preparing to (Re)design a financial product.

Congratulations, you’ve just taken over an underperforming savings product, and have been directed to improve its performance. The market research is complete, and have chosen a persona to start with, unmarried, early career savers.

It seems likely they would be the early adopters for new digital features and the market size and potential of this group of customers seems promising. Time to set up a meeting with the boss and colleagues to gain buy-in for your plan and make magic happen.

Step 1: Strategic Alignment and Planning

Thanks to your research and financial analysis, you’re nearly ready to put your team together and begin the design work. All you need is to:

- Gain buy-in for your target persona (unmarried, early career savers)

- Agree on a target behaviour to change (save regularly)

- Set a target outcome (Net Deposit Growth/Revenue Contribution)

Success! You set aside 90 minutes for this high-stakes strategic meeting. You answered the big questions and crafted the Behavioural Challenge Statement providing a clear goal for the product team you’re about to assemble. This challenge statement provides both a means to test the effectiveness of your product designs to come, and a mission for the team, something that orients the whole team to the challenge at hand, a product North Star.

Here’s an example: How might we help customers make small and regular deposits into a savings account so that they can save all of their digital small change and we can earn more deposits?”

Congratulations, the strategic exercise is complete!

Your business undergoing digital transformation making it easier to access individuals from multiple teams; operations, retail banking, marketing, and of course design. You’ve got 8 people in total, but since the engineers from IT have their hands full just now, you decide to run product design sprints, rather than developing in parallel.

You’ll meet every day at the same time and use a lower resolution means of testing product designs, called usability testing, just to spot potential problems (bugs) with your design and give you an early sense for probability of success. You’ve secured physical meeting space, created a team communication channel for asymmetric communication, and a standing meeting invite link, you’re ready to go!

Step 2: Map

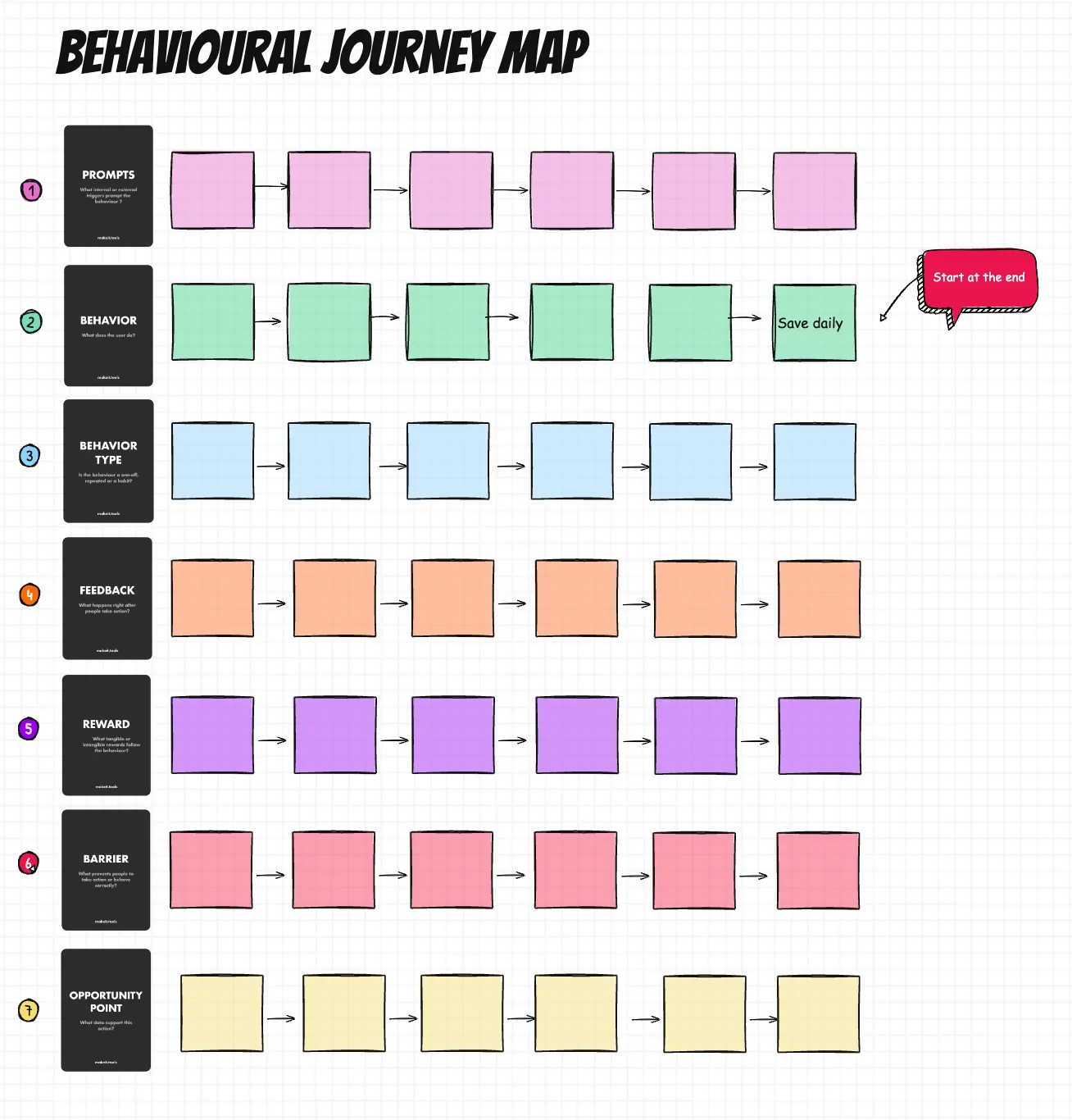

Mapping is the first day of the sprint, and it’s all about building the team's shared understanding of the target audience and their choice environment. It involves presenting the behavioural challenge statement, research about your target audience, and the journey map showing the steps leading up to the target behaviour. Note, a behavioural journey map considers key insights stemming from the 5 laws of behaviour (see Figure 2)

Leveraging customer research completed before the sprint, you know that saving more money for emergencies and for major purchases (e.g., vacations and first homes) is an important financial goal for this audience. You have been trained in behavioural design using the Make it behavioural design framework, so your journey map is more detailed than traditional journey maps. It considers key insights stemming from the 5 laws of behaviour, like what happens just before and right after the action? What does the choice environment look like? And most importantly, which barriers might prevent the target audience from taking the steps that will lead to a goal.

During this first day, the team identifies many barriers that prevent the target audience from achieving their goals. One in particular stands out as potentially the most viable to further work on - this consumer rarely pays for their purchases with cash, preferring to use their mobile phone, card, or smartwatch. They Lack a Prompt to save every day.

Individuals in later life stages have learned to save by accumulating the small change they came home with, an experience that digitally savvy younger savers lack. This change would accumulate over a period of time, resulting in an occasional deposit of the accumulated change at a local bank branch. In most instances, carrying that small change was cumbersome to carry and inconvenient for making larger payments with, resulting in it being what we call an environmental barrier for pre-digital individuals, a friction that helped with saving, younger, digital savers lack this. The team identifies two frictions, a lack of prompt at account opening (they are not asked about their savings goals), and prompt to save the small daily change as they transact.

After running a prioritization exercise to drill down even further (e.g., Planning Poker), you determine that the barrier of concern is a missing prompt for daily savings. Congratulations you’ve successfully completed Mapping!

Step 3: Brainstorm

The team sits back down and brainstorms ideas to help the target audience save money every day. Reviewing the Make it strategy cards, as the behavioural design expert in the team, you had recommended two tactics that looked promising and set the team to work sketching how they might be able to use a Default Option and Temptation Bundling.

The meeting concludes with the team individually presenting their ideas visually, some did this with sketches on paper, other did it with stickies, but great ideas (and some less great ideas) were shared by all. Congratulations you’ve successfully completed Idea Generation!

Step 4: Design

On day 3 of the sprint, the team shortlists the best designs and gets to work building a wireframe, a mockup or an interactive prototype to test with the target audience. They made this decision by playing the prioritization game - Planning Poker, allowing individuals to make assessments of the difficulty in building the feature and potential benefits. As Product Manager you decide on two individual features to build and test.

There are hundreds (sometimes thousands) of new bank accounts opened nationwide every day, so you decide to give Financial Advisors of branches located near three universities across the country a new sales script that offers a free savings account in addition to the account they came into open. These two accounts would allow the bank to “automatically” transfer funds from a checking account to a savings account (for the initial test, these transfers would be completed manually). This was enough to formulate a design hypothesis.

“ If we bundle a free savings account that automatically rounds up customer-initiated debit transactions to the nearest dollar, and then transfer the difference between the purchase and the rounded up amount to a savings account, then target customers should be able to save $100/year, which will should grow the balances by $10 million over the next year.”

In building this initial design, the team focused on two simple features, the sales script for branch Financial Advisors, and what came to be called the sweep function, a software feature that allowed for transactions to be automatically rounded up to the nearest dollar in order to be transferred. The sales script was straightforward.

“We recommend you also open a savings account with no service charges, this account allows you to automatically transfer the change generated by your purchases into a savings account, it’s like a piggy bank, would you like this service?”

The sweep would take some effort, the account software the bank used did have this function, but having not been used for this purpose previously, it would take some time to configure, so the team decided that to test this feature, they would open 100 accounts and manually transfer the funds for two months every day. In this way, there would be no engineering effort, and no design effort, Product details were already available on both accounts, so no marketing effort was required. However, this was for all intents and purposes a functional prototype.

Step 5: Test

You wanted to be confident that the script and sweep function were responsible for the additional savings, and that your results were unbiased (it is always possible that the young savers that agreed to this would anyways have saved more money then average), so you decided to run an A/B test, one group would have the sweep function, and the others would simply be asked if they would like to open a savings account as well.

The results of the test were very promising. The young savers averaged 25 transactions per month which resulted in roughly $15 being moved into the savings account (against an average of $4/month being moved into savings in the control group). This projection suggested that young savers would save $180 per year, which would result in $18 million in new deposits from this target audience, and these results were available within the first 90 days of being in your role, a pretty outstanding first quarter result!

There were some additional discoveries during this test that helped the team refine the product. A financial calculator showing projected savings increased signup for the two accounts, because it made the value proposition clearer for the young saver, and a fee added with withdrawals at the ATM made savings stay longer in the account (a goal shared by both the young saver and the bank). As a little bonus, we looked into the future and saw that 5 years after this product was launched, the bank had raised an additional $180 million in deposits, a spectacular result!

If you want to know more about using Make it behavioural design in your product, reach out to us!